Property News

New private home sales fell in April 2025 amid US tariffs concerns and dearth of OCR launches; The city fringe led sales – spurred by Marina South project

Developers’ sales fell in April, with 663 units (ex. EC) sold in the month – down by 9.1% from March 2025. Year-on-year, sales more than doubled from the 301 units transacted in April 2024.

New home sales in April were led by the Rest of Central Region (RCR), where 551 new units (ex. EC) were sold.

New private home sales dipped in April, with 663 units (ex. executive condos) sold in the month, due to fewer mass market new launches and concerns over the US tariffs. Month-on-month, this represented a 9.1% decrease from the 729 units transacted in March. However, on a yearly basis, sales more than doubled from the 301 units shifted in April 2024.

Developers put up 1,344 new units (ex. EC) for sale in April, representing a 142% increase from the 555 units launched in March. Three new projects were launched in the month: the 358-unit Bloomsbury Residences in Media Circle; the 937-unit One Marina Gardens in Marina South; and the 19-unit freehold luxury boutique development 21 Anderson. The former two projects collectively sold 491 units and accounted for 74% of monthly new home sales.

Rebounding from lower sales last month, the Rest of Central Region (RCR) saw 551 new units sold in April, more than six times higher than the 87 units in March. It was not unexpected that this sub-market led sales in April, given that two new launches - Bloomsbury Residences and One Marina Gardens - are located in the RCR. Sales were mostly contributed by One Marina Gardens, which sold 384 units at a median price of $2,948 psf, while Bloomsbury Residences moved 107 units at a median price of $2,454 psf. Other RCR projects such as Grand Dunman and The Continuum also continued to pare down on unsold units, selling 14 units and 11 units, respectively in April.

Meanwhile, the Outside Central Region (OCR) made up 14% of new home sales in April, with 95 units (ex. EC) sold. This is a sharp 84% fall from the 596 units transacted in March, and is the lowest monthly sales tally in 14 months since the 58 OCR units transacted in February 2024. The steep decline in sales in April can be attributed to the lack of OCR new launches, as new sales in March and February were boosted by the launch of Lentor Central Residences and Parktown Residence, respectively. The best-selling OCR projects in April were Parktown Residence and Lentor Mansion, which moved 17 units at a median price of $2,368 psf and 12 units at a median price of $2,183 psf, respectively.

Over in the Core Central Region (CCR), developers’ sales remained relatively tepid, with 17 new units sold in April - representing a 63% decline from the 46 units shifted in March. This is the slowest monthly sales in the CCR since September 2024, where 15 new units were transacted in this sub-market. The CCR projects that topped sales in April were Hill House which sold four units at a median price of $3,017 psf, and 21 Anderson which transacted three units at a median price of $4,811 psf.

In the EC market, developers sold 96 new units, markedly lower than the 781 units transacted in March when Aurelle of Tampines was launched. Riding the strong sales momentum from the previous month, Aurelle of Tampines continued to lead EC sales in April – moving 54 units at a median price of$1,764 psf. As at end-April, 52 units of unsold new ECs remained on the market; the limited EC supply is likely to support sales at the upcoming launch of Otto Place EC in Tengah which could come on in the second half of 2025.

In April, foreigners (non-PR) made up 2.4% of new private home sales (ex. EC), the highest proportion in four months. According to caveats lodged, there were 16 transactions from foreign buyers (NPR), with the majority from One Marina Gardens which had 10 such transactions. Meanwhile, there were two transactions at Watten House, and one each at Bloomsbury Residences, Lentor Central Residences, Parktown Residence and The Myst by foreigners (NPR). Singapore PRs and Singaporeans made up 12.0% and 85.5% of the non-landed new private home sales (ex. EC), respectively in April (see Chart 1).

Based on caveats lodged, 71% of the units sold at Bloomsbury Residences were priced at below$2,500 psf, while on a price quantum basis, nearly 92% of the units were sold at below $2.5 million (see Table 1). Meanwhile, the units sold at One Marina Gardens fetched higher $PSF prices, starting upwards of $2,700 psf, but a sizable portion of sales at 84% were still priced at below $2.5 million. Right pricing and quantum play remain a key selling strategy for developers in future launches, with units priced below $2.5 million being the pricing sweet-spot for many buyers.

At the luxury development 21 Anderson, all three units sold in April were transacted at above $20.5 million, with unit prices crossing $4,600 psf.

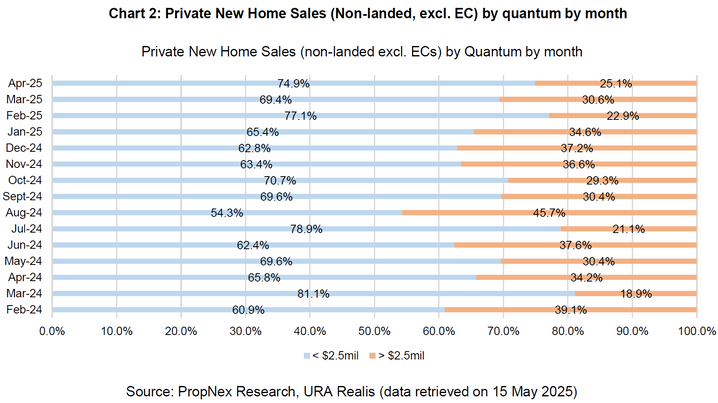

According to URA Realis caveat data, about 74.9% of new private non-landed homes (ex. EC) sold in April were priced at below $2.5 million, up from the 69.4% proportion in March (see Chart 2). The median transacted price of non-landed private new homes (ex. EC) sold in April was about $1.98 million, slightly lower than $1.99 million in the previous month, based on caveats lodged.

Outlook

In the coming months, developers’ sales may increasingly be driven by the CCR and RCR, amidst a limited number of OCR launches. PropNex expects new home sales to be subdued in May, as there have been no new projects being launched thus far.

While the US tariffs have introduced uncertainty into the market, the situation is evolving and recent US-China talks have led to a significant dial back of trade tariffs for a 90-day period. The de-escalation in US-China trade tensions will offer some temporary reprieve, although underlying volatility remains. Meanwhile, PropNex is cautiously optimistic about the private housing market in Singapore, in view of the stable demand for homes, the tight labour market, as well as a relatively manageable level of unsold inventory, which stood at 18,125 units (ex. EC) in Q1 2025. For comparison, the number of unsold uncompleted private homes during uncertain times previously was at 29,149 units in Q1 2020 when the Covid-19 pandemic struck, and at around 43,000 units in 2008 amidst the global financial crisis.

Based the sales data, developers sold 4,038 new private homes (ex. EC) in the first four months of 2025, about 62% of the 6,469 new units transacted in the whole of 2024. Supported by the ample supply of new launches lined up, PropNex is retaining its projections for new home sales at 8,000 to 9,000 units (ex. EC) for 2025. With more CCR and RCR projects in the pipeline for 2025, PropNex also anticipates that overall private home prices may potentially climb by 3% to 4% in 2025.